2017 is just around the corner. A recent Student Loan Hero survey revealed that paying off debt is so far, the most common financial resolution of 2017. Next to getting out of debt is building an emergency fund. Through personal experience getting rid of my own debt and through helping many clients pay off their credit cards and loans, I’ve learned this: reducing your debt cannot be accomplished without strategic planning. For most people, the accumulation of debt takes years. It is most likely not going to be resolved in a fingers snap. So, although deciding to radically pay off your debt in 2017 is a great decision, if you do not set an organized and intelligent plan, it is going to be a failed attempt at being debt free. The good news is that by December 2017, your financial position can be totally different.

Only 8% of people reach their goal after setting new year’s resolution. Why? It’s not for lack of desire; I believe it’s just for lack of planning and discipline. This year, let’s beat those bad odds. You can reach your goal in 2017 and you will.

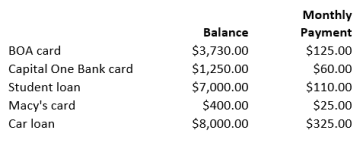

First, determine how much you owe.

The first step toward having a successful resolution this year is to be aware of where you stand financially. What are you starting with? People say ‘I want to get out of debt’ but they don’t even know how much debt they have. It is important to be specific. Grab a sheet of paper and start listing your credit cards and loans with their respective balances along with the minimum monthly payments. Your list may be similar to the following:

You currently owe $20380 and your monthly minimum payments add up to $645. This is your starting point. You are no longer in a fog, hoping to soon find a beaming light that will guide you to your destination. You now have a path and a direction to follow.

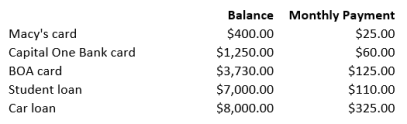

Second, organize your debt list from the smallest to the largest balance.

Third, implement the following strategy to reducing or paying off your debt in 2017.

The reason for organizing your debt from the smallest to the largest balance is to start tackling the smallest amount first. There are theories and other thought-processes on the ‘right’ way to handle debt but I believe starting in this case with Macy’s is the smartest choice. I recently read an article which recommended to always pay more than your minimum payments, thus allocating a larger amount toward your principal balance. In some instances, it is the right move. However, there are times when trying to get out of debt while maximizing every single monthly payment would be very hurtful and would bring you even deeper in the debt hole. Why? I explain it below. If you have enough cash to proceed with large payments toward your different credit accounts, you shouldn’t be in debt to start with.

I’ll use a sport analogy to illustrate my philosophy. In soccer, there are teams such as the ‘Gli Azurri’ (Italy’s national team) which have an impenetrable defense. They usually play the entirety of their matches protecting their goalkeeper and win by surprising the opponent with a destroying counter attack. However, that often becomes a detriment when the opponent finds its way to Italy’s goal posts. This happened on July 2, 2000 during the final of the UEFA (European Cup). Italy scored first and then played a defensive strategy the entire match. At the 93rd min (in extra time), France equalized and went on to win the cup. There are also teams that have incredible offensive players but are crippled when their defense is shaken up by the opponent. In any sport, the best teams are the ones that master both the art of defensive tactics and the art of offensive plays. To get out of debt, you must learn the art of offensive and defensive money management.

Beside sticking to your goal and being disciplined while reducing your debt, it is very important is to increase your cash reserve aka ‘your savings’ aka ‘your emergency funds’. While you’re paying off debt, you need to gradually increase your cash on hand. Why? You had accumulated the debt because you did not have cash. Moreover, what good is it to use that credit card that you’re trying to pay off when an emergency arises? In that case, you simply operate a revolving door.

Let’s go back to the example above for practical illustration. You are required to make payments in the amount of $645 at a minimum. Imagine that your budget allows you to put $900 toward your debt. Your goal to is to pay off your smallest credit card balance (Macy’s) as fast as possible. You now have $255 available. In addition to the $25 minimum payment, instead of distributing the $255 across your other credit cards and loans, save about $100 and add the remaining $155 to your Macy’s payment. Doing so, you are increasing your cash reserves while putting more toward the principal on the smallest credit card (or loan) balance. Continue making the regular payments on your other debt units during this period. Very soon your smallest debt will be a thing of the past. Once your Macy’s card is paid off, you now have $25 (the minimum payment) and the other extra $155 to allocate to the next smallest debt: your Capital One Bank card. Your payment toward your Capital One card goes from $60 to $240 ($60+$155+$25) while you’re still saving about $100 every month. You may even increase your savings if you would like. In a few months, you Capital One credit card will be at a zero balance. Next, simply add the $240 to your $125 monthly payment to Bank of America.

I hope you are now seeing where this leads. While it may seem like you are not making progress on your large units of debt at the beginning, your payments towards them increase at an exponential rate.

*Credit card vs. Loans: prioritize credit cards over loans. Your loans have fixed rate and a specific due date. On the contrary, interest is compounded on your credit cards’ balances. When trying to get out of debt, make sure your credit cards are first paid off prior to increasing your monthly payments on loans.

By applying this strategy in 2017, you will defensively increase your cash reserve while offensively decrease your debt.

2017 is here. This year is your year to be financially stable.

Leave a comment